This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

By 2026, it plans to nearly triple its audit rates for large corporations with assets exceeding $250 million. Under these plans, partnerships with assets over $10 million will also see audit rates increase tenfold by 2026. The post How Your Business Can Prepare For and Respond to an IRS Audit appeared first on Roger Rossmeisl, CPA.

Its generally limited to eligible employees who begin working for the employer before January 1, 2026. The post Understanding the Work Opportunity Tax Credit appeared first on Roger Rossmeisl, CPA.

With this date getting closer each day, you may wonder how your federal tax bill will be affected in 2026. appeared first on Roger Rossmeisl, CPA. Our current situation The Tax Cuts and Jobs Act (TCJA), which generally took effect in 2018, made sweeping changes. Many of its provisions are set to expire on December 31, 2025.

compound annual growth rate and hit a new high at 98 million units in 2026. The post The Auto Industry is Likely to Decline in Enterprise Value appeared first on Roger Rossmeisl, CPA. According to IHS Markit, during the next five years unit auto sales will increase at a 4.7%

It’s generally limited to eligible employees who begin work for the employer before January 1, 2026. The post Work Opportunity Tax Credit Provides Help to Employers appeared first on Roger Rossmeisl, CPA. The IRS recently issued some updated information on the pre-screening and certification processes.

law made changes that will allow more people to be eligible for these accounts, beginning in 2026. The post Disabled Family Members May Be Able to Benefit from ABLE Accounts appeared first on Roger Rossmeisl, CPA. The SECURE 2.0 Anyone can contribute to an ABLE account. While contributions aren’t tax-deductible, the funds in the.

Beginning on January 1, 2026, the amount is due to be reduced to $5 million, adjusted for inflation. Don’t Overlook Income Taxes appeared first on Roger Rossmeisl, CPA. Important: Keep in mind that the federal estate tax exclusion amount is scheduled to sunset at the end of 2025. The post Planning Your Estate?

Beginning on January 1, 2026, the amount is due to be reduced to $5 million, adjusted for inflation. The post Your Estate Plan: Don’t Forget About Income Tax Planning appeared first on Roger Rossmeisl, CPA. Note: The federal estate tax exclusion amount is scheduled to sunset at the end of 2025.

Rahill, CPA/PFS, JD, LL.M., 1, 2026, and—absent new legislation before then—will revert to approximately $7 million for individuals and $14 million for married couples, subject to inflation adjustments. Rahill, CPA/PFS, JD, LL.M., million for individuals and $27.22 million for married couples).

The looming sunset of the expanded lifetime estate and gift tax exemption will arrive on January 1, 2026. As of January 1, 2026, the current lifetime estate and gift tax exemption will be cut in half and adjusted for inflation. Key Takeaways: As of 2024, the lifetime estate and gift tax exemption stands at $13.61

The Illinois CPA Society (ICPAS)—one of the largest state CPA societies in the nation—is proud to formally announce its new board of directors for the April 1, 2023, to March 31, 2024, fiscal year. The board welcomes three new directors serving through March 2026, including Lindy R. Rodrigo, CPA, CGMA, partner at Roth & Co.

According to a license lookup, Jerkins (we can’t stop laughing at that name given the context) received his Tennessee CPA license in 2015. It is currently active until 2026. JBS had office locations in Fairview and Nashville, Tennessee.

The Ohio Society of CPAs announced yesterday that their state is leading the way in alternative pathways to CPA licensure, officially. 8, which includes OSCPA-backed legislation that will position Ohio as a national leader in addressing the dire CPA shortage. This is exactly what the AICPA was afraid of.

Beginning with tax year 2025—filing for which happens in early 2026—Coloradans will be able to use the IRS’s free Direct File program to submit their state and federal taxes online for free.

office space will be vacant by early 2026, according to a new report from Moody’s and first reported by Bloomberg. By Sarah Lynch, Inc. TNS) The office is getting emptier—and will soon reflect the new world of work. Twenty-four percent of U.S. That’s up from the 19.8 percent reported in in the fourth quarter of 2023.

For those living on a fixed income such asSocial Security, a key part of financial planning may include keeping tabs on next years cost of living adjustment, and right now theyre looking pretty low.

That’s generous by historical standards but in 2026, the exemption is set to fall to about $6 million ($12 million for married couples) after inflation adjustments — unless Congress changes the law. The post How to Ensure Life Insurance Isn’t Part of Your Taxable Estate appeared first on Roger Rossmeisl, CPA. million ($23.4

The credit is generally limited to eligible employees who began work for the employer before January 1, 2026. The post Work Opportunity Tax Credit Extended Through 2025 appeared first on Roger Rossmeisl, CPA. Generally, an employer is eligible for the credit only for qualified wages paid to members of a targeted group.

Thats a principle weve come to live by here at Padgett & Padgett, PLLC CPA. – Tax year 2025 (reporting in 2026): 2.5K – Tax year 2026 (reporting in 2027) and after: 600 dollar threshold. What the 1099-K Requirements Mean for Your Skagit County Small Business Change is inevitable, except from a vending machine.

A family office focuses on managing the wealth and the personal affairs of a family, typically through the services of a large CPA firm. With the implementation of TCJA, that deduction has been suspended until 2026. What exactly is a family office?

Artifact of PwC’s Women’s Consulting Experience landing page from Google search The five entry-level PwC programs listed right now are Career Preview, Start Internship, Destination CPA, Advance Internship, and While You Work – CPA Acceleration Program. Preferred major GPA: 3.3

Brad Stumpe, CPA, CRCM , partner and compliance and loan review practice leader, hosted a webinar, HMDA Refresher Including What Reporters Must Know Prior to Section 1071 Implementation , to inform financial institutions of their obligations under HMDA reporting requirements.

The ASB issues standards for auditing private companies, quality management standards for practitioners providing audit and attest services to private companies, and attestation standards.

1, 2025, and prior to Jan 1, 2026. Senate Bills 167 and 175 will significantly change the impact of credits and NOLs that Taxpayers had been planning to use in 2024 or later, and 2024 estimates must be reevaluated to consider the impact of these changes for the 2024 – 2026 tax years. 1, 2024, and prior to Jan. 1, 2024, and before Jan.

The Auditing Standards Board issues standards for auditing private companies, quality management standards for practitioners providing audit and attest services to private companies, and attestation standards.

For tax years beginning in 2026, individual taxpayers who itemize their deductions will once again be able to deduct miscellaneous expenses to the extent that those expenses together exceed 2% of their AGI. The Section 199A deduction is set to expire after 2025, for Tax years beginning in 2026, the 199A deduction will no longer be available.

Individual rate caveats: The QBI deduction is scheduled to end in 2026, unless Congress acts to extend. appeared first on Roger Rossmeisl, CPA. The post Choosing a Business Entity: Which Way to Go?

For the 2024 tax year, the threshold is $5,000, though reductions are expected in 2025 and 2026 The IRS initially planned to lower the reporting threshold to $600, but implementation has been delayed.

In 2026, the standard deduction will return to pre-TCJA levels. The TCJA suspended the Pease rule, but it is scheduled to return in 2026. The rules are set to revert to the pre-TCJA structure in 2026 with a $1,000 credit. Now the previous rules will be reinstated in 2026. It is now set to be in reinstated in 2026.

The final regulations announced today will require brokers to report gross proceeds on the sale of digital assets beginning in 2026 for all sales in 2025. Brokers will be required to also report information on the tax basis for certain digital assets beginning in 2027 for sales in 2026,” the Treasury Department said in a news release.

Banks will need to prepare for these finalized CRA requirements, which will go into effect in stages beginning on April 1, 2024 , and continuing on January 1, 2026 and January 1, 2027. These new thresholds do not go into effect until January 1, 2026 : Small banks will be those with total assets of less than $600 million.

Update 2024-03 states that the amendments are effective for public business entities for annual reporting periods beginning after December 15, 2026, and interim reporting periods beginning after December 15, 2027. In the proposed ASU, the FASB says: The Board issued Accounting Standards Update No.

For reporting on Scope 1 and 2, data from FY 2025 will be used to report in 2026. Reporting on Scope 3 will be effective as of FY 2027, reporting on FY 2026 data. Reporting for SB-261 will be required on or before January 1, 2026 which will be before SB-253. Reporting is required annually using a digital reporting platform.

The IRS decided on the $11 fee by estimating that the cost of providing PTINs for fiscal year 2024 through fiscal year 2026 was $27,432,969, including labor and benefits; travel, training, and supplies; and overhead. contractor fee may change in 2026 when the current contract expires and will be recomputed, according to the IRS.

This requirement was scheduled to take effect in 2024, but the IRS has postponed it until 2026 to accommodate administrative needs of employers (Notice 2023-62, 8/23/23).

Over 200 entities made up of Fortune 500 companies, firms, and public employers, including the American Retirement Association, Chipotle Mexican Grill, Fidelity Investments, Charles Schwab, Microsoft Corporation, and Delta Airlines, asked Congress for a two-year delay to the Roth catch-up rule to 2026.

Revenue projections vary by scenario, ranging from $45 million to $112 million for 2026, to between $59 million and $160 million for 2030. The state estimates each Washington resident could make between 42 and 46 online retail orders for delivery in 2026. The state anticipates administrative costs will increase by 1.5%

Robert Hamilton Reappointed as GASAC Chair Mr. Hamilton’s second term as GASAC chair will continue through December 31, 2026. He is a certified public accountant (CPA) and received his degree from the University of Oregon. Suzanne Lowensohn to the role of vice chair for the GASAC.

Notice 2024-73 also announces that the final regulations the Treasury Department and the IRS plan to issue for 401(k) plans on long-term, part-time employees will apply no earlier than to plan years beginning on or after Jan. A proposed regulation related to the rules for long-term, part-time employees in 401(k) plans was issued on Nov.

Generally, these forms will be sent separately to taxpayers and the IRS in early 2026, the agency said. The IRS on Aug. 9 unveiled an updated draft version of Form 1099-DA , which cryptocurrency brokers will use to report certain sale and exchange transactions of digital assets that take place beginning in calendar year 2025.

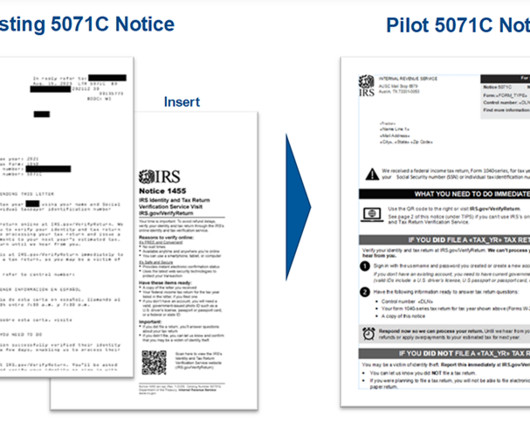

The redesign work will accelerate during the 2025 and 2026 filing seasons, improving common IRS letters going out to individual taxpayers and then expanding into notices going to businesses. The IRS will be actively engaging with taxpayers and the tax professional community to gather feedback on how these notices should be redesigned.

State CPA Society News & Updates is a round-up of recent announcements and initiatives by CPA associations in the United States and its territories. The Kentucky Society Certified Public Accountants (KYCPA) announced their newest board members, whose terms began in July 2023 and will continue through 2026.

Starting April 2025 these rates will reduce to 30% and 35%, before returning to their original rates of 20% and 25% in April 2026. For orchestras, the rate will remain at 50% until April 2025, then reducing to 35% before returning to the original rate of 25% in April 2026.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content