This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

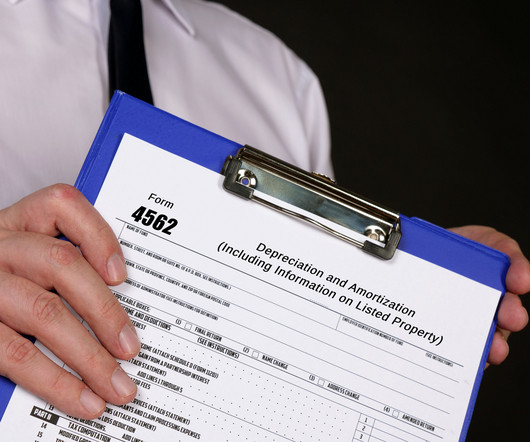

If, during the tax year, a client has purchased a tangible or intangible asset and is looking to claim depreciation and amortization deductions or expense certain property under Section 179 , Form 4562 must be filed with their annual taxreturn. Any depreciation on a corporate income taxreturn (other than Form 1120-S).

Unfortunately, the complexities and the time it can take to manually input business clients’ asset information, especially when onboarding new clients, means added work and stress in an already busytax season. The business owner can then deduct a portion of the equipment’s declining value from their taxes.

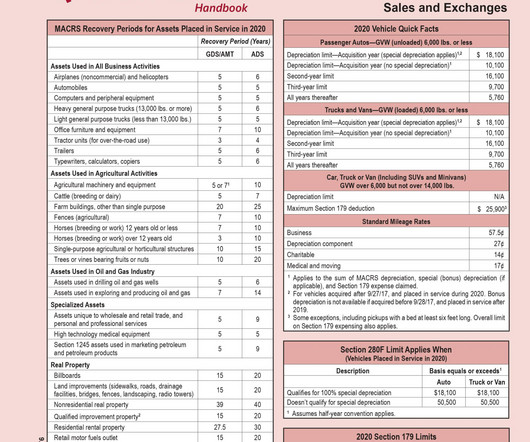

When enacted, bonus depreciation enabled businesses to immediately write off 100% of the cost of eligible property acquired and placed in service after Sept. Book The trusted tax depreciation guide book from Thomson Reuters Checkpoint® Shop the Depreciation Quickfinder Handbook How does depreciation work in an S corporation?

This means electric cars costing over £40,000 will pay an (at current rates) extra £355 per year on top of the normal road tax of £165 per year. The benefit in kind tax for electric cars is going up to 5% by 2027/2028, with an increase of 1% per year taking effect in 2025/2026 until the 5% level is reached in 2027/2028.

The tax credit rates are 60% for eligible capture equipment used in a direct air capture project, 50% for all other eligible capture equipment and 37.5% for eligible transportation storage and use equipment with lower tax credit rates applicable from 2031 to 2040. Introduction of the Critical Mineral Exploration Tax Credit (CMETC).

Any adjustment needed for a 2022 federal income taxreturn already filed which included the capitalization of research and experimental expenditures can either be amended or, at the taxpayer’s election, be treated as an automatic change in the method of accounting in the 2023 taxable year.

The deadline for submitting the San Francisco Gross Receipts Taxreturn is quickly approaching on February 28, 2025. A broad restructuring of the exemption threshold, apportionment formulas, and rates could considerably change your tax liability and estimates required for 2025. They are scheduled to increase in 2027 and 2028.

The depreciation percentage will continue to decrease 20% each year until bonus depreciation is no longer available for property placed in service in 2027. Planning should occur with your tax advisor on how to optimize bonus depreciation. C corporation pays to add $0.94

Depending on the auto dealership that is chosen, an individual may not have to wait until the filing of their income taxreturn to benefit from the credit. Most dealers will need to rely on the prior year’s taxreturn filings to ensure the credit is allowable and therefore can be properly claimed by the dealership.

Depending on the auto dealership that is chosen, an individual may not have to wait until the filing of their income taxreturn to benefit from the credit. Most dealers will need to rely on the prior year’s taxreturn filings to ensure the credit is allowable and therefore can be properly claimed by the dealership.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content