This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Companies that apply and are accepted into this program can benefit from various tax benefits, such as: PaLife Sciences Investment Tax Credit (90% refundable) (pursuant to M.G.L 63, 30(17)) Designation as R&D Corporation for Sales Tax Purposes (pursuant to M.G.L. 62, 6(m) and c. 62, 6(n) and c. 62, 6(m) and c.

And unfortunately, its not mostly the fun stuff keeping you busy its things more on the housekeeping side of running your business, like meeting tax and other important government deadlines. Monday, March 17 : S corporation and partnership taxreturns are due for calendar-year businesses. Whats in it for you?

Additionally, the tax filer cannot be a full-time student and cannot be claimed as a dependent on another person’s taxreturn. Beginning in 2027, the recently enacted SECURE Act 2.0

“The final regulations ensure that taxpayers will receive statements that include information reported to the IRS on Form 1099-DA, Digital Asset Proceeds from Broker Transactions , that will help them file their income taxreturns and determine their tax obligations.

If a business timely filed its original 941s and no fraud is involved, then the IRS has until April 15, 2024 to deny 2020 claims, it has until April 15, 2025 to deny Q1 and Q2 2021 claims, and it has until April 15, 2027 to deny Q3 and Q4 (for recovery startup businesses) 2021 claims.

How long does the IRS have to audit your return? Generally, the “statute of limitations” for audits is the later of three years from the date your return is filed or the taxreturn due date. Therefore, the deadline for 2023 returns is usually April 15, 2027. Ignorance is not bliss.

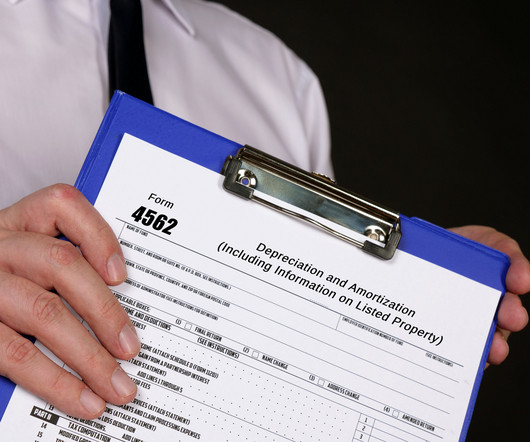

If, during the tax year, a client has purchased a tangible or intangible asset and is looking to claim depreciation and amortization deductions or expense certain property under Section 179 , Form 4562 must be filed with their annual taxreturn. Any depreciation on a corporate income taxreturn (other than Form 1120-S).

This will replace the need for a Self-Assessment taxreturn. Making Tax Digital from April 2026. Making Tax Digital from April 2027. Those with an income of between £30,000 and £50,000 will need to do this from April 2027. Read more of Inform's tax blogs : Struggling to pay tax – What should you do?

This will apply to corporate taxpayers with taxable income exceeding $100,00 for taxable years beginning on or after January 1, 2022, through taxable years beginning on or after January 1, 2027. For taxable years beginning 2022, the top corporate tax rate is 7.5%; For taxable years beginning 2023, the top corporate tax rate is 7.25%; .

In most cases, the IRS can audit, propose adjustments, and assess additional tax up to 3 years after the later of (a) the date a return was filed or (b) the original due date. For example, assume your 2023 individual taxreturn was filed on April 11, 2024, a few days before the due date of April 15, 2024.

According to a recent report by the Institute on Taxation and Economic Policy , the TCJA expanded tax breaks for “accelerated depreciation” have reduced taxes by nearly $67 billion for “the 25 profitable corporations that benefited the most, based on information disclosed by the companies themselves.” 27, 2017, and before Jan.

Without AII (applying the half-year rule): First-year CCA deduction: $1,000 × 27.5% = $275 First-Year Deduction With AII for purchases from November 21, 2018 to December 31, 2023: With AII (suspending the half-year rule plus an additional 50% of the CCA): First-year CCA deduction: $1,000 × 55% X 1.5 = $825 Additional tax deduction of $550 First-Year (..)

Anything of an ongoing or permanent nature can be transferred to a more permanent file after your taxreturn is completed and filed. Having all your new documents together when you have your return prepared can jog your memory and could lead to a tax benefit. Do the same with digital files.

The business owner can then deduct a portion of the equipment’s declining value from their taxes. In this scenario, the owner could deduct $1,000 each year on taxreturn for depreciation. This results in tax savings for that business owner. 1, 2027, unless the law changes. 1, 2027, bonus depreciation is eliminated.

The 100% bonus depreciation is also allowed for specified plants planted or grafted after September 27, 2017 and extended to before January 1, 2027. The 100% bonus depreciation will decrease by 20% per each taxable year beginning after 2022 and expires January 1, 2027. Technical Correction on QIP Under Cares Act.

taxreturns for the 2022 tax year. The Act retains 20% bonus depreciation for property placed in service after December 31, 2025, and before January 1, 2027. This may be administratively problematic for companies that have already filed their U.S.

Pass-through entities like a sole proprietorship, partnership or S-corp, won’t see the benefits as any charitable donation made by those businesses will pass through to your personal taxreturn. C-corps are allowed to take a deduction on the business for charitable distributions, which can potentially reduce their taxable income.

Online marketplace sales are expected to exceed $603 billion in the United States in 2027, or nearly 35% of all U.S. By 2027, marketplaces may account for 59% of ecommerce globally. Some states require marketplace facilitators to identify their own sales separately from third-party sales on their sales taxreturns.

This means electric cars costing over £40,000 will pay an (at current rates) extra £355 per year on top of the normal road tax of £165 per year. The benefit in kind tax for electric cars is going up to 5% by 2027/2028, with an increase of 1% per year taking effect in 2025/2026 until the 5% level is reached in 2027/2028.

A head start in addressing any tax-related concerns arising from the transaction can highlight options for tax planning actions the company may take before year end and ensure a smoother process for tax provision and taxreturn preparation for 2023. and foreign taxes should review their strategies annually.

Bonus depreciation has been declining by 20% each year and will be zero for property placed in service in 2027 (60% in 2024 and 40% in 2025). The typical year-end tax planning point is to defer income and accelerate expenses where possible.

The IRS has posted a June 2021 draft version of the Form 941 , Employer’s Quarterly Federal TaxReturn, instructions that take into account the amended and expanded coronavirus (COVID-19) pandemic tax credits and the new COBRA premium assistance credit from the American Rescue Plan Act (ARPA). Federal News.

In 2023 bonus depreciation will decrease to 80% and continue to decrease 20% in each of the following years until bonus depreciation is no longer allowed in the 2027 taxable year. Other cost segregation services include: Look-back studies to recapture depreciation deductions from prior tax years without amending your taxreturn.

However, they have advised that taxpayers will either need to go back and amend the earlier years on completion of the accounts or that an adjustment may be included in the following tax year. Transition period. Transitional period is a loss.

For property placed in service after December 31, 2025, and before January 1, 2027, bonus depreciation would remain at 20%. Tax practitioners are likely weighing the potential of extensions because of the high belief that this bill will pass with retroactive measures. For the 2023 taxable year, a 179 expense of $1.16

The tax credit rates are 60% for eligible capture equipment used in a direct air capture project, 50% for all other eligible capture equipment and 37.5% for eligible transportation storage and use equipment with lower tax credit rates applicable from 2031 to 2040. Introduction of the Critical Mineral Exploration Tax Credit (CMETC).

But if you take that into a QuickBooks Desktop discontinuance even with the sun setting, it means all of the Intuit QuickBooks Desktop products except enterprise would be gone by 2027. And, of course, we’ve seen the transition from prosystem tax into excess tax and so forth.

The deadline for submitting the San Francisco Gross Receipts Taxreturn is quickly approaching on February 28, 2025. A broad restructuring of the exemption threshold, apportionment formulas, and rates could considerably change your tax liability and estimates required for 2025. They are scheduled to increase in 2027 and 2028.

Any adjustment needed for a 2022 federal income taxreturn already filed which included the capitalization of research and experimental expenditures can either be amended or, at the taxpayer’s election, be treated as an automatic change in the method of accounting in the 2023 taxable year. billion.

Can I outsource other personal tax work? HMRC expects around 2 million taxpayers will use the MTD IT service by 2027. This means another 10 million taxpayers will still need to submit self-assessment taxreturns in the usual way by 31 January after tax year-end.

The depreciation percentage will continue to decrease 20% each year until bonus depreciation is no longer available for property placed in service in 2027. Planning should occur with your tax advisor on how to optimize bonus depreciation.

Throughout MTDs phased implementation, weve been supporting accountants to digitalise records and transition away from paper-based taxreturns, supporting compliance while introducing efficiencies and minimising the risk of errors. Those with an income over 30,000 will be mandated from 2027.

Take that deduction away, their taxes could be as high as $37,000 on that income. One item we have seen as a significant issue for many businesses with significant capital expenditures is the drop in bonus depreciation from 100% in 2022 to 0% in 2027.

Depending on the auto dealership that is chosen, an individual may not have to wait until the filing of their income taxreturn to benefit from the credit. Most dealers will need to rely on the prior year’s taxreturn filings to ensure the credit is allowable and therefore can be properly claimed by the dealership.

Depending on the auto dealership that is chosen, an individual may not have to wait until the filing of their income taxreturn to benefit from the credit. Most dealers will need to rely on the prior year’s taxreturn filings to ensure the credit is allowable and therefore can be properly claimed by the dealership.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content