This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Mistakes happen, especially when it comes to recording transactions in your books. One type of accounting mistake thats easy to make is a transposition error. Read on to learn what is a transposition error and how it can affect your accountingbooks. What is a transposition error?

Learn how to record the types of revenue in different accounts. That way, you can keep your accountingbooks updated, organized, and legal. When you make a sale or earn money from another activity, you need to record it. What is revenue? Revenue, or sales, […] READ MORE.

Understand the difference between tangible vs. intangible assets to keep your accountingbooks and financial statements accurate. All businesses have assets. Assets can be broken down into two categories: tangible and intangible. Tangible vs. intangible assets Both tangible and intangible assets add value to your business.

Your accountingbooks should reflect how much money you have at your business. If you use double-entry accounting, you also record the amount of money customers owe you. When it comes to your small business, you don’t want to be in the dark. But, what happens if they don’t pay?

Knowing how much inventory you have is crucial for managing accurate small business accountingbooks, ordering new stock, and making pricing decisions. Unless you own a service-based business, you likely have inventory. So, what is inventory? Your small business’s inventory […] READ MORE.

Accounting errors are inevitable, especially if you’re rushing to add information into your small business accountingbooks. To detect accounting errors sooner rather than later, learn how to find accounting errors.

There are many different accounts you can use to record equity in your business accountingbooks. Before you can begin tracking equity, you must learn about the different types of equity that can apply to your company.

But, how do you record these tax collections and payments in your accountingbooks? Sales tax accounting. You should understand accounting for sales tax to maintain organized and accurate […] READ MORE. When you sell goods to customers, you likely collect and remit sales tax to the government.

As a small business owner, setting up your accountingbooks and maintaining accurate records is essential. To make that happen, you need to be familiar with accounts payable and accounts receivable. What is the difference between […] READ MORE.

Learn about deferred revenue and how to record it in your accountingbooks. Do customers pay you for your goods or services before you actually deliver them? If so, you need to know about deferred revenue. What is deferred revenue?

Referring to your bank statements or accountbooks separately cannot help you to summarize your transactions and balance. Even if you forget to enter any transactions to your accountbook, bank reconciliation statements might help you figure out the correct balance. Supports you in making financial decisions .

In contrast, accrual accounting records transactions when they occur, offering a more accurate depiction of the company’s financial position over time by matching revenues with expenses. BookAccounting and Tax Accounting Small businesses may notice differences between bookaccounting and tax accounting.

Improve cross-department data sharing and visibility Today there’s a greater need for real-time visibility between departments that handle tax and GAAP accountingbooks. Real-time documentation ensures you always have the crucial information you need for complex audits and other data management demands.

As negative as the IRS’ reputation is, it has to be said that they give Los Angeles, or Orange County business owners and taxpayers more than enough prior notice to get their accountingbooks in order, so there really is no excuse for missing a tax deadline.

They will then work with your business to achieve the accounting tasks. Reduce errors and achieve accuracy Accounting tasks can make minor errors that could cause problems when analyzing the accountingbooks. Outsourcing your accounting is a way to reduce mistakes and improve accuracy.

Introducing the Father of Accounting The next item is an accountbook cover from 1343 from the Italian City of Siena (Gallery 307). The Father of Accounting is recognized to be Fra Luca Pacioli, who incidentally was a friend of Leonardo da Vinci. Pretty exciting stuff, Huh? More excitement!

As a small business owner, you track the money your company earns in your accountingbooks. As a small business owner, you need to account for your company’s […] READ MORE. Can you identify the types of income you record? For example, ordinary income is a common type of income that your business earns.

As a small business owner, you might not be an accounting wizard, but your math needs to add up. To discover and get to the root of errors in your double-entry accountingbooks, use a trial balance. If you use accrual accounting to manage your books, your credits […] READ MORE.

When you manage your accountingbooks by hand, you are responsible for a lot of nitty-gritty details. One of your responsibilities is creating closing entries at the end of each accounting period. What are closing entries?

You must know the fair market value of your assets to maintain accurate small business accountingbooks, obtain outside […] READ MORE. And when you sell those assets or buy new ones, you should know their fair market value.

Having accurate accountingbooks is essential for making financial decisions, securing financing, and drafting financial statements. But sometimes, you find gaps in your records, either from making mistakes or carrying out transactions from one accounting period to another.

When you run a small business, one error in your accountingbooks can result in inaccurate financial statements, poor cash flow management, and even an IRS audit. To make sure your records are accurate, familiarize yourself with account reconciliation. What is account reconciliation?

Unplanned expenses, like inventory shrinkage, can lead to a drop in profits and require you to alter your accountingbooks. When running a business, you likely face setbacks due to unforeseen costs. And […] READ MORE.

However, you could end up collecting debts you write off in your accountingbooks. When you offer credit to customers, you may need to write off unpaid receivables as bad debts. If this happens, record the money as a bad debt recovery. What is bad debt recovery? Bad debt recovery, or bad debt collection, is […] READ MORE.

If that is not the case, you will need to take steps to clean up accounting records or use a catch-up bookkeeping service. . When and Why You Need to Clean Up Your Books. There are many reasons to have clean accountingbooks each month. Here are a few: Ensure Financials Are Up-to-Date.

It’s time pre-order the most valuable fraud investigation and forensic accountingbook you will ever read. I had the privilege of previewing Leah Wietholter’s book Data Sleuth: Using Data in Forensic Accounting Engagements and Fraud Investigations. She has knocked this one out of the park.

This may include: Business income and expense records Bank statements and canceled checks Receipts for business expenses Accountingbooks and ledgers Prior years’ tax returns The Audit Process: For correspondence audits, you’ll mail in the requested documents. Preparation : Gather all requested documents.

In business, keeping accountingbooks – records of all the financial operations of your business – is a must. Nowadays the process is made easier by high-quality accounting software which eases the strain of heavy responsibilities.

TSG’s lawsuit filed last August in Los Angeles District Court said that Fox had promised TSG a share of defined gross receipts for pictures under the companies’ long-term participation agreement but that the studio used “nearly every trick in the Hollywood accountingbook” to not pay.

Make sure you simplify managing your business by using Synder – the best solution for your accounting. Synchronize your payment data in your accountingbooks and receive error-free reconciliation and customized categorization. Start accounting ASAP.

Attestation ledger : A register or accountbook created to provide support/ evidence of individual transactions. Block explorer : A tool people use to view all cryptocurrency transactions online. Block reward : The number of cryptocurrency coins a person gets if they successfully mine a block of the currency.

Record transactions in accountingbooks. All business accounts are recorded in your accountingbooks. Of course, accountingbooks aren’t real books, as they used to be back in the day. If you’re using a single entry method, you record your income and expenses in a cash register.

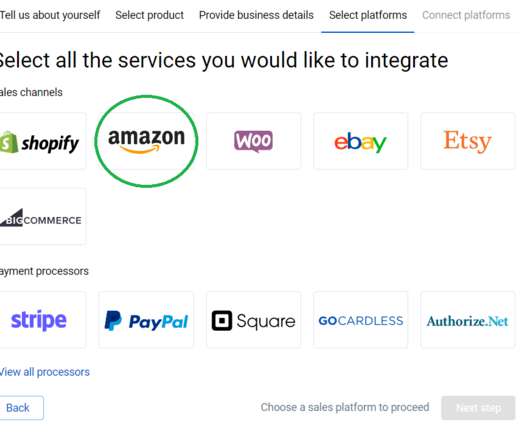

To help you even further, you can set up product mapping which will automatically sync the product names in sales channels with those in your accountingbooks, saving you the headache of tracking and correcting uncategorized or miscategorized products. Customer support.

With Synder, you can synchronize transactions to your accountingbooks with just one click and get 100% precise reconciliation. If you subtract your liabilities from your assets, you’ll get your business’ shareholder equity. Cash-flow statement. Cash-flow statements are almost like your real-time income statements.

Even in the 21st century, it’s still possible to do your bookkeeping with paper spreadsheets or accountbooks. If manual accounting works for you, nobody can force you to change. Accounting standards are the same whether you use ledgers or laptops.

That’s what almost all accountingbooks are about. Learn more about how Synder can simplify your e-commerce business and check the features or schedule a Demo session with Synder’s specialists. . What is an expense report used for? Business owners must keep records of every penny spent on their company’s expenses.

You debit the $12,500 to AR and credit the same amount to your sales account. This is known as balancing your accounts/books. You recognize this in your accounting with a “bad debt” entry. When the customer pays, you credit $12,500 to AR and debit cash.

It records all your sales and fees into your accountingbooks, getting an error-free profit and loss report and balance sheet. The data sync engine brings all the necessary details including amounts, customers, and shipping addresses to make sure your books are perfect.

The accountantbooked a short initial series of weekly mentoring sessions. It was only quite recently that they decided to increase the size of their client base so have only just started networking to build relationships and generate referrals.

This ensures accurate data imports and that there are no duplicates in your accountingbooks. Synder Sync uses the most detailed transactional information including time stamp, amount, billing address, and more. Find a dropshipping center.

So you’ll need to either consult your accountant or have neat accountingbooks to file Tax reports on your own. Simple steps to start your business automation. What’s Amazon automation? It’s the ability of your business to work and make a profit even if you’re not working on it.

With product mapping , you can categorize different products across all your sales channels and bring them neatly into your accountingbooks, the way you see fit. With the rules , you can assign product categories, product names, fee categories, and perform many other helpful data operations.

It means that you’ll have to ensure your online payment data is correctly reflected in your accountingbooks, no transactions are missed, and each part of a transaction belongs to the right category in the books.

To avoid that, you can set up Product Mapping with Synder, where you can link 2 product names together so that they’re recognized and recorded as the same item in your accountingbooks.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content