This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Finance teams planning for their year-end financialstatement audit have an even longer list of things to think about at the end of the year, including income statements, balance sheets, and, finally, the income tax provisions and disclosures that must be presented in the financialstatements.

Restatements of financialstatements and management reports on internal control over financial reporting (ICFR) that were audited by the firm over the past three years. This business model is a complete mismatch for the complexity auditors need to master in todays environment to achieve suitable levels of audit quality.

The scheme included Dellomo’s submission of a “false and misleading” management representation letter to Lovesac’s outside auditor, according to the lawsuit. The accounting problems came to light in April 2023, when Lovesac’s finance team found that approximately $2.2 Meanwhile, Lovesac continues to expand its reach.

During verification, it was observed that in the Financialstatements of the company for 2016-17, 2017-18, and 2018-19, the directors did not mention DIN under their signatures. The RoC imposed a penalty of INR 18,00,000/- (INR 6,00,000/- per year) on company directors for failure to mention DIN on Financialstatements.

“Audit firms and preparers alike emphasized that they are continuing to explore various ways of integrating GenAI-enabled tools in auditing and financial reporting.” audit regulator recently spoke to auditors who work at the U.S. Evaluating the completeness of financialstatement disclosures.

Check out Accountingfly’s top remote accounting candidates of the week and sign up for Always-On Recruiting to get a new batch of accountants and auditors for hire in your inbox every week — free! But in recent months, local governments have been waiting longer and paying more for required financialstatements.

One of the most common errors made by executives in a small startup is assuming that the reporting basis for accurate financialstatements can be changed by clicking the single button at the top of the QuickBooks report. The issue is that auditors don’t arrive only after the fiscal year has been closed.

Assuming no one but select audit partners actually read this crap, let’s take a look at how auditors should expect increased vigilance in 2024 so everyone can be better informed and stock up on KY. You’ve been warned, auditors. Next up, culture. They snag a decent fish every now and then, sure. Anyway, firm culture.

The Public Company Accounting Oversight Board (PCAOB) introduced on Wednesday a new series of staff guidance, “Audit Focus,” that is intended to provide easy-to-digest information to auditors, especially those who audit smaller public companies, with critical audit matters (CAMs) as the first topic.

In a letter to auditors on Wednesday, ASIC announced it would soon commence a new data-driven surveillance of auditor independence and conflicts of interest. Some have gone as far as to call for auditors – particularly the “big four” – to be banned from offering consulting services to their audit customers.

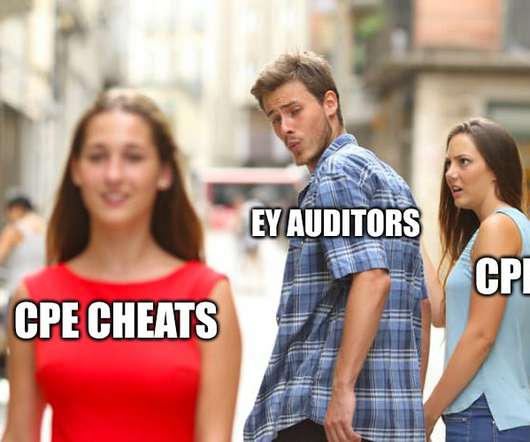

With the EY cheating scandal making headlines even outside of our precious little accountosphere we decided to take a look at the full SEC order to answer the question — how and why were EY auditors cheating on CPE exams? The long and short of it is, EY auditors trying to shortcut CPE took advantage of a software exploit.

Market concentration in the consultancy industry came to a head this year after it was revealed PwC partners had misused information by passing on confidential Federal Government information to clients, sparking the sale of its consulting business to Allegro Funds to $1. Such suggestions are false.

However, my role is not just to teach the material but to excite them about accounting as a profession and auditing in particular and share my pride in the vital role auditors play in our ecosystem. In its simplest form, auditors provide an opinion on an organization’s financialstatements. Ethics is not a buzzword.

Statutory reporting is a critical process for multinational corporations, involving the preparation and submission of financialstatements to comply with legal obligations across various jurisdictions. Key components of statutory reports include financialstatements and ESG disclosures, enhancing stakeholder trust and governance.

As these companies gain traction and seek external investments, audited financialstatements play a crucial role in instilling trust among stakeholders, investors, and potential partners. 10 Key Steps Here are the key steps startup e-commerce companies can take to prepare for their audited financialstatements.

The Public Company Accounting Oversight Board (PCAOB) approved a sweeping new standard on the general responsibilities of an auditor on May 13, including a provision that significantly cuts the maximum time period for the auditor to assemble a complete and final set of audit documentation from 45 days to 14 days.

There is a brand-new section that debuted today in PCAOB inspection reports of audit firms, and it is devoted to auditor independence. “We These enhancements will provide relevant information that investors have asked for and support improvements in overall audit quality.”

Auditors, like so many others today, are seizing the opportunity to transform how they work by adopting artificial intelligence. These findings make it critical for those of us in the audit profession to help the next generation understand the vision and opportunities that await those who choose this career path as auditors embrace AI.

The SEC has fined EY a record $100 million after an investigation revealed auditors at EY were cheating on ethics exams (open book ethics exams we presume) and CPE; worse than cheating alone, they actively tried to cover it up and hide the cheating from the SEC. Well this is bad. Hodgman, Associate Director of the SEC’s Enforcement Division.

The Public Company Accounting Oversight Board (PCAOB) has recently adopted a significant new auditing standard, AS 1000, titled “ General Responsibilities of the Auditor in Conducting an Audit.” AS 1000 updates key auditor responsibilities, emphasizing their role in protecting investor interests with independent reports.

As financial reporting complexities grow, firms must adapt their methodology and maintain clear, detailed records that demonstrate compliance with these evolving standards. With step-by-step procedures, practical checklists, and real-world examples, auditors at all levels can navigate complex engagements with confidence.

Those of us who’ve worked or even simply seen behind the curtain of audit know the things he points out to be true — assurance is reasonable not absolute , financialstatements are the responsibility of management not auditors, “finding fraud” is not the ultimate goal of audits — but do investors?

But with a year of remote inspections under their belt, the PCAOB hinted that inspectors were picking nits more during the 2021 inspection cycle, which probably wasn’t good news to firms that are already understaffed and auditors who are already overworked—a recipe for disaster (hence all the mistakes inspectors found). In Part I.B

The lead-up: Choosing auditors and timing. The audit probably took about 25% of my time personally — maybe even more once the auditors arrived.” What types of auditors are there, and how do you choose one? How do you decide what auditor to choose? KELLY: “The auditors will ask about processes and controls.

” However, when it comes to financialstatement audits, the timing isn’t quite as forgiving as planting trees. Understanding the dynamics of your financial health is crucial for early-stage tech companies. One such decision is when to conduct a financialstatement audit. The second-best time is now.”

In the ongoing scandal of Wirecard , under fire for fraud, the focus is now turning to auditors Ernst & Young (EY), which reportedly failed to report Wirecard’s “unorthodox financial arrangements” as far back as 2016, The Wall Street Journal (WSJ) reported.

Accounting automation platform Trullion announced its Audit Suite, a cloud-based solution designed for auditors to leverage artificial intelligence to enhance accuracy and reduce human error in audits. Audit Suite allows auditors to centralize and streamline their process. More information on Trullion Audit Suite can be found here.

The firm messed up on one of its nine audits inspected, and it pertained to the financialstatement audit only. If you include the last time Cohen & Company auditors screwed up an audit, which was in 2017, that’s two mistakes in the last 43 audits inspected, for a deficiency rate of 4.6%. and in the world.

Often, the blame is cast in the direction of the auditors. The auditors are an easy target. Not only do they usually have professional liability insurance policies to fall back on, the auditors initially seem like the logical culprit. The mistake management makes is in believing that a financialstatement audit will find fraud.

Today, ESG is resulting in significant opportunities for auditors, fueled by the widening range of stakeholders calling for ESG prioritization, an influx of laws and regulations pertaining to ESG, and a rise in ESG investment products. Other ESG matters may not have any material effect on the financialstatements.

Auditors are poised to become crucial facilitators in the accounting and finance function’s adoption of AI and large language models (LLMs). Auditors are the Keystone for AI Integration The successful integration of AI has one essential requirement—a nuanced understanding of the model’s data origins and its interpretations.

Amidst the noise, lets separate the hype from reality and explore how GenAI can genuinely enhance an auditors daily life and work. Hype vs reality: GenAI use cases for auditors With its promise of immense benefits and time-savings, todays auditors would do well to explore the opportunities of embracing GenAI.

One of the most common errors made by executives in a small startup is assuming that the reporting basis for accurate financialstatements can be changed by clicking the single button at the top of the QuickBooks report. The issue is that auditors don’t arrive only after the fiscal year has been closed.

The PCAOB on Tuesday introduced a proposal amending current PCAOB auditing standards related to the auditor’s responsibility to detect noncompliance with laws and regulations, including fraud, in the audit of a public company. The proposal also makes explicit that financialstatement fraud is a type of noncompliance with laws and regulations.

Even with all the publicity surrounding the issue of financial fraud in the last twenty years, most auditors, investors, and other professionals still do not “get it” when it comes to detecting fraud. Traditional financialstatement audits were never designed to detect fraud. Nothing could be further from the truth.

WSJ: The widening shortage of accountants has begun showing up in financialstatements. ” “In the course of completing the preparation of the quarterly financialstatements for the Form 10-Q, the Company determined that it had a deficiency in the Companys internal control over financial reporting as of April 22, 2023.

A rules proposal issued by the Public Company Accounting Oversight Board (PCAOB) on June 26 addresses aspects of designing and performing audit procedures that involve technology-assisted analysis of information contained in electronic format.

Are you having trouble finding remote accountants, CAS experts, auditors, or tax professionals for your firm or internal team? Drop your information here , and we’ll reach out to schedule a call to discuss how Accountingfly can work for you. Accountingfly can assist you! Sign up now to find your next hire.

During verification, it was observed that in the Financialstatements of the company for 2016-17, 2017-18, and 2018-19, the directors did not mention DIN under their signatures. The RoC imposed a penalty of INR 18,00,000/- (INR 6,00,000/- per year) on company directors for failure to mention DIN on Financialstatements.

I am scheduled to present four free webinars primarily for CPAs, but anyone in business that uses financialstatements might also find them interesting and insightful. I also discuss the importance of checklists and preplanning that will allow the auditor to have more focus and better manage their precious time.

Business owners and finance teams equipped with information on potential audit triggers can approach the process with greater confidence, viewing it as a manageable annoyance, rather than a daunting burden. However, knowledge is power. Though close attention to detail in the reporting process may seem tedious, it doesn’t have to be.

By providing accuracy and remaining compliant, A&E firms can demonstrate their commitment to financial management and reporting, attracting new clients who value these qualities. A: An independent third-party auditor typically conducts an overhead rate audit. Q: Who conducts an overhead rate audit?

Auditors rely on data review to ensure the reliability and integrity of financialstatements. Auditors must ensure that financialstatements are free from material misstatements and that all relevant information is included. It helps auditors identify errors, irregularities, and potential fraud.

For 2021, GT ’s audit failure rate is right around its most recent five-year average: Our 2021 inspection report on Grant Thornton LLP provides information on our inspection to assess the firm’s compliance with Public Company Accounting Oversight Board (PCAOB) standards and rules and other applicable regulatory and professional requirements.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content