This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Barclays recently announced the companies picked for its Tel Aviv accelerator program, according to reports, and while officials at the banks touted a focus on payments security, the bank has also targeted corporate payments in its startup batch. Of the 2,000 startups that applied to join the Barclays Accelerator program , just 40 were accepted, the bank’s head of open innovation, Arian Lewis, recently told Finance Magnates.

It’s no secret that, as fraudsters continue to evolve and increase the sophistication of their tactics, the fraud prevention landscape must do the same in order to stay one step ahead. In an effort to show some recognition to the “good guys” out there and the innovative efforts being made to disrupt their respective marketplaces, Gartner has identified the recipients of this year’s “Cool Vendor” recognitions.

Though it’s an officially discouraged practice among drivers, Uber has been burning rubber with ambitious partnerships and service expansions over the past few months. What happens when Uber runs out of road to innovate on, though? It goes aquatic. Uber confirmed to CNN on Friday (April 29) that it would embark on a new venture in Dubai over the weekend where a chartered yacht will ferry a lucky dozen riders through the Middle Eastern city’s waterways.

When looking for evidence as to why in-store mobile payments haven’t taken off (a hot topic in Karen Webster’s column this week), there are a number of factors to consider but only one real guiding principle: certainty. Consumers need to know that they can use that method of payment where they like to shop and that it will work the same way each and every time.

Your financial statements hold powerful insights—but are you truly paying attention? Many finance professionals focus on the income statement while overlooking key signals hidden in the balance sheet and cash flow statement. Understanding these numbers can unlock smarter decision-making, uncover risks, and drive long-term success. Join David Worrell, accomplished CFO, finance expert, and author, for an engaging, nontraditional take on reading financial statements.

Walmart is open — not just for business but to new technology ideas. After several years spent trying to infuse its multi-billion dollar business with more forward-thinking concepts with mixed results , last week, the retail giant announced that it will be conducting what amounts to an open call for tech innovation. It is looking to startups to potentially lead growth with big ideas and new technology solutions from small, agile companies.

Online merchants know very well that fraud costs them in many ways – in chargebacks, in false positives, in the friction that’s introduced at checkout that can cost a sale. But there’s nothing like putting the cost of fraud into the parlance that merchants know really well: units sold. Something that Kount says its data shows that merchants must make eight additional sales to make up for the cost of one fraudulent order.

Misery loves company, or so the saying goes. And while one could perhaps quibble with the exact phrasing there — misery probably, more accurately, likes company but would, on the whole, only love not being miserable anymore — the recent run of numbers in retail certainly brings the old adage to mind. While not quite every retailer took a beating — Amazon had a great quarter, Walmart logged solid results, TJX continued its winning streak and Urban Outfitters and H&M managed to find ways to ke

Misery loves company, or so the saying goes. And while one could perhaps quibble with the exact phrasing there — misery probably, more accurately, likes company but would, on the whole, only love not being miserable anymore — the recent run of numbers in retail certainly brings the old adage to mind. While not quite every retailer took a beating — Amazon had a great quarter, Walmart logged solid results, TJX continued its winning streak and Urban Outfitters and H&M managed to find ways to ke

Like many developing areas, Latin America holds promise for payments companies and the burgeoning movement to digital transactions in lieu of coins and paper bills. In an interview with PYMNTS, Alexander Sjogren, YellowPepper’s CTO, stated that his firm has evolved beyond its initial underpinnings in the mobile banking services segment focusing on underbanked and underserved populations.

[link]. In the age of sophisticated cyberfraud, and more specifically fraudulent payments, it’s not enough for cardholders around the globe to wait till their statements arrive in the mail (paper or electronic) and ferret out suspicious activity. By then the damage has been done, the trail has run cold. To that end, TSYS, the global payments solutions provider, said earlier this month that it has begun offering its cardholder alerts solution to its clients based in Europe, with an eye on pushing

After a few years of speculation — and a couple of fairly notable wrong guesses — the real creator of bitcoin has been identified — mostly because he identified himself. Australian entrepreneur Craig Wright has stepped forward and admitted to being the real “Satoshi Nakamoto.” Apart from the claim, Wright has also submitted proof in the form of coins known to be owned by bitcoin’s creator.

Starbucks and Dunkin’ have cracked it. Walmart Pay seems to have all of the ingredients to do it, too. Facebook and Messenger could but haven’t yet. Android Pay has acknowledged that it’s critical to its success and its latest announcements suggest they are working on it. Visa and MasterCard could totally nail it. We don’t know enough about Chase Pay’s plans to be able to say one way or the other.

Traditional budgeting and forecasting methods can no longer keep pace with today’s rapidly evolving business environment. Static budgets, rigid annual forecasts, and outdated financial models limit an organization’s ability to adapt to market shifts and economic uncertainty. To stay ahead, finance leaders must leverage a future-forward approach—one that leverages real-time data, predictive analytics, and continuous planning to drive smarter financial decisions.

Over the weekend, CBS brought FinTech to prime time during a segment of its “60 Minutes” broadcast on Sunday (May 1). The program offered an exciting and broad overview of how startups in the space are using technology to innovate the delivery of payments and financial services. Lesley Stahl, who hosted the segment, used Stripe as an example of how FinTech is transforming payments and, in particular, how they simplify the process new merchants face when attempting to accept payments online.

Paper checks. Foreign exchange rates. Settlement times. All points of pain and friction in cross-border payments and all factors that can stymie cash flow for firms and even the smallest sole proprietors or freelancers that operate in a global, always-on economy. Earlier this month, GoldMoney , a FinTech that operates a financial services and payments platform that uses gold to settle transactions globally in any currency, launched its Gold Payroll and Gold Payout applications.

The latest stats released by MasterCard give more optimism about the U.S. EMV adoption rate by merchants and issuers. And for today’s Daily Data Dive 5-in-1, PYMNTS has broken those stats down: 1.2 Million | The number of chip-active merchant locations as of April 30, 2016. 121 | The percentage increase in EMV-enabled merchant locations since the Oct. 1 deadline. 67 | The percentage of U.S.

If you think of the rise of corporate America over the last century, the function of the accounts payable department probably doesn’t come to mind as one of the main players. But something has happened over the last few years, according to Coupa VP of Strategy and Product Marketing Donna Wilczek: Technology has enabled AP professionals to become strategic and massively important to the success of any corporation, large or small.

As businesses increasingly adopt automation, finance leaders must navigate the delicate balance between technology and human expertise. This webinar explores the critical role of human oversight in accounts payable (AP) automation and how a people-centric approach can drive better financial performance. Join us for an insightful discussion on how integrating human expertise into automated workflows enhances decision-making, reduces fraud risks, strengthens vendor relationships, and accelerates R

The digital banking industry is heating up — and fast. That’s why, in the May edition of the PYMNTS Digital Banking Tracker™ , we’ve profiled 58 players from the FinTech and consumer banking space, including 10 additions to the Tracker: CashControl, CSI, Finex Banking Solutions, HelloWallet, Innofis, Kony, Money Lover, SilverWiz, The One Place Capital Limited and Q2 Software, Inc.

Banks may not always be up for overhauling their operations with a largely untested, disruptive technology, but new reports suggest the threat of fraud in one area of corporate finance is encouraging financial institutions to adopt distributed ledger technology in growing volumes. Reports by Bloomberg on Sunday (May 22) said banks are examining ways to protect themselves against fraud in the trade finance sector, worth $4 trillion in today’s market.

Remember when you first asked Siri some silly question only to receive a response that indicated she was onto your shtick and potentially not as thoroughly amused by it as you were? That, as it turns out, was the good old days of voice technology assistance. Today the incorporation of voice technology into daily activities runs the gamut, from taking music requests on-demand to ordering from Amazon to typing your texts for you.

“Siri, help me find the nearest Starbucks.”. “Hey Cortana, play some yacht rock.”. “Alexa, pay cable bill.”. This month’s Digital Banking Tracker™ cover story features an interview with Ed Metzger, Santander UK’s Head of Innovation about their early feedback from incorporating a voice assistant into their student-focused SmartBank app – and what’s next for voice technology in banking.

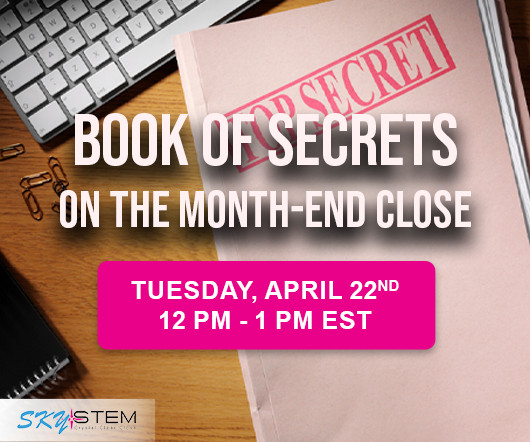

Based off SkyStem's popular e-Book, the book of secrets to the month-end close will be revealed in this one-hour webinar. Learn leading practices when it comes to building a strong and sustainable month-end close that has room to grow and evolve. Learn about the power of precise estimates, why reconciliations are critical to closing the books, how and when to automate, and how the chart of accounts play into your close process.

Let’s check in with who’s on the AI (artificial intelligence) train. Apple kicked things off this year, announcing back in January that it had purchased Emotient, an AI tech startup in the facial recognition business. Did Apple say why it bought that company? Of course, it did not ; mind your own business. Jump ahead to spring, and the next big company in the retail space (specifically, the biggest company in eCommerce) to make an AI-related move this year was Amazon.

We don’t have to look far to see the ways in which cartoons and comics of the past – with their futuristic tools and services – are influencing the advancing technologies we see hitting the market today. Though we may not have reached the threshold of flying cars and warp drives just yet, robotics are quickly starting to change the ways in which humans approach many different aspects of our everyday lives.

Although the traditional retail industry in the U.S. continues to struggle mightily , surely there are verticals within it that are largely immune to such troubles by sheer virtue of the fact that they trade in essential items … right? Sort of, but also — not exactly. If we break down “essential items” into three categories — food, clothing and shelter — we’re looking at a trio of verticals wherein each one has still had to weather the storm of the current retail climate in its own way.

President Barack Obama and his administration get a lot of demands, to say the least. Stop ISIS, bring peace to the Middle East, clean up the economy, create more jobs, fix the education system, lower taxes, etc., etc. Of course, that’s just what comes with the territory. One thing that’s probably not higher on that rapidly growing list?

AI is reshaping industries, yet finance remains one of the slowest adopters. Concerns over compliance, legacy systems, and data silos have made finance teams hesitant to embrace AI-driven transformation. But delaying adoption isn’t just about efficiency—it’s about staying competitive in a rapidly evolving landscape. How can finance leaders overcome these challenges and start leveraging AI effectively?

There’s a new app in town that wants to make it easier to remember to pay those credit cards. Or as its co-founder Jason Brown told Mashable : “It’s kind of like a self driving car for your credit card.” Yes, the apps have taken over. And it has one goal: making sure those credit card companies don’t slap the consumer with another late fee again.

Chief financial officers have a lot on their plate — from ensuring an entire company is financially viable to managing activities that make that company not only efficient but also profitable. A day in the life of the CFO in 2016 looks drastically different from just five or 10 years ago. With a significant shift away from manual processes and the onset of new technologies, a CFO’s responsibilities have broadened to encompass more than simply managing the P&L.

“Too many people start to have an imagination about ‘nirvana’ or the ‘perfect transaction’ – but that’s a science experiment.” It’s true, the idea of perfection in payments may be a bit far-fetched, but if there’s no actual “nirvana” then what is everyone striving for? In a Fireside chat with MPD CEO Karen Webster at this year’s PYMNTS Innovation Project , Paul Galant, Verifone CEO , said it’s really about the day-to-day efforts of delivering efficiency,

Mobile payments. Two words that, when combined, arguably couldn’t be hotter. While one has become the standard for how much of the world’s population connects to the Internet — and, thereby, each other — the latter has transformed these same devices into the “mobile wallets” that connect those same people to goods and services, often without lifting a finger to complete transactions.

Is your tech stack working for you—or are you working for it ? 🤖 In today’s world of automation and AI, technology should simplify workflows—not add complexity. Seamless integration and interconnectivity are key to maximizing productivity, optimizing workflows, and improving collaboration. Join expert Joe Wroblewski for a practical and insightful session on how you can build a smarter, more connected tech stack that drives efficiency and long-term success!

The only way to predict what the emerging payments trends are for today is to seek out the one group of people who has the power to control the entire market: consumers. But, of course, no two consumers are exactly alike – especially when comparing consumers across different regions of the world. To truly understand how consumers think and act on a global scale, talking to them about their payments preferences is the only way to help those who’d like to influence that behavior seems pretty

Some of the largest financial institutions came out this week with new statistics on small business sentiment in the U.S. Bank of America, Capital One, Wells Fargo, Chase and more published their findings — sometimes to contradicting conclusions. Small business sentiment is perhaps the most mixed and muddled metric. Chase reached some optimistic conclusions regarding how small business owners feel about the year ahead, while Capital One highlighted a 9 percent decline in SME optimism.

Bringing Wearables To The POS Frontline. What if merchants could wear the POS? No joke. Merchants have seen the benefits of “line busting” solutions that put mPOS tablets in the hands of a sales associate or employee. But in the May edition of the Developer Tracker, powered by Vantiv, Jeremy Feldman, CEO of stealth startup LibriSpark , shared his vision for how merchants can now take this to the very next level: making POS not only mobile, but wearable.

ATM skimming just got taken to the next level. Kaspersky Lab announced new research regarding a hacker collective, known as the Skimer group, that uses malware to essentially make an ATM steal users’ money. Instead of putting skimmer devices on the ATM, this group makes the entire ATM a skimming device. This program was first discovered in 2009, but researchers have now discovered that the malware is being reused to attack banks around the world.

Finance isn’t just about the numbers. It’s about the people behind them. In a world of constant disruption, resilient finance teams aren’t just operationally efficient. They are adaptable, engaged, and deeply connected to a strong organizational culture. Success lies at the intersection of people, culture, adaptability, and resilience. Finance leaders who master this balance will build teams that thrive through uncertainty and drive long-term business impact.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content