This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Sales tax is full of complexities, but there are certain topics that seem to cause more of a headache than others. Drop shipments are one of those topics. As e-commerce continues to explode – it almost doubled during the pandemic and was already rising sharply nationwide in early 2019 – drop shipment transactions have become even more prevalent. Many companies have added marketplaces on websites and don’t maintain their own inventory for online purchases.

RESOURCES / ARTICLES. Exciting Clients…. with Review Meetings! Accountants interpret financials to advise clients, sometimes through ‘quarterly [or monthly] review’ meetings. How do we get clients excited (and willing to invest) in these meetings? They need to see the value and believe in the approach. Then they’ll enter productive, long-term advisory relationships.

When applying for government contracts, it’s important to understand the types of contract options that are available to you. Each type of contract carries its own risks and opportunities and can help you make decisions when compiling your proposal. Project managers should work closely with their team to manage resources, track the project’s performance to budget, and communicate with the accounting department to review billing rates to make sure the contract remains profitable.

What if you decide to, or are asked to, guarantee a loan to your corporation? Before agreeing to act as a guarantor, endorser or indemnitor of a debt obligation of your closely held corporation, be aware of the possible tax consequences. If your corporation defaults on the loan and you’re required to pay principal or interest under the guarantee agreement, you don’t want to be blindsided.

Traditional budgeting and forecasting methods can no longer keep pace with today’s rapidly evolving business environment. Static budgets, rigid annual forecasts, and outdated financial models limit an organization’s ability to adapt to market shifts and economic uncertainty. To stay ahead, finance leaders must leverage a future-forward approach—one that leverages real-time data, predictive analytics, and continuous planning to drive smarter financial decisions.

For any business, the worst thing that can happen is that you can find yourself in a 911 urgent tax help situation. The IRS is known to be the toughest and most ruthless of all collection agencies on the planet. If you ever find yourself in trouble with the IRS, never consider going it alone. There are always avenues for you to turn and they do allow you to have a representative on your side.

Important efficiency metrics for SaaS startups include Sales Efficiency (aka the Magic Number), Human Capital Efficiency, and Capital Efficiency. The post 3 Important Efficiency Metrics for SaaS Startups appeared first on Burkland.

Is it just your imagination or is e-commerce expanding every year? It’s not your imagination. Let’s see some numbers : 5% of global internet users have purchased products online. The e-commerce industry is growing 23% year-over-year (yet 46% of American small businesses still don’t have a website). By 2040, an estimated 95% of all purchases will be through e-commerce.

Is it just your imagination or is e-commerce expanding every year? It’s not your imagination. Let’s see some numbers : 5% of global internet users have purchased products online. The e-commerce industry is growing 23% year-over-year (yet 46% of American small businesses still don’t have a website). By 2040, an estimated 95% of all purchases will be through e-commerce.

Small businesses are making the leap into digitalization to respond to evolving consumer behavior and expectations, adapting to new working norms, putting data to work to drive performance and building business resiliency. The post 4 Reasons Why Digital Transformation Is Table Stakes for Small Businesses appeared first on Xendoo.

As posted to the Lex Fridman YouTube Channel on 8/20/21 (Run Time: 11 min, 29 sec) “Tesla AI Day presented the most amazing real-world AI and Engineering effort I have ever seen in my life” — Lex Fridman On 8/19/21, Elon Musk convened Tesla AI Day, an event to share progress in the automaker’s software and hardware development related to artificial intelligence.

You know that paying someone comes at a cost. In addition to giving employees their paychecks, you also have the cost of payroll taxes. So, how much does an employer pay in payroll taxes? Keep reading to learn more about the employer cost of payroll taxes. How much does an employer pay in payroll taxes? […] READ MORE.

As businesses increasingly adopt automation, finance leaders must navigate the delicate balance between technology and human expertise. This webinar explores the critical role of human oversight in accounts payable (AP) automation and how a people-centric approach can drive better financial performance. Join us for an insightful discussion on how integrating human expertise into automated workflows enhances decision-making, reduces fraud risks, strengthens vendor relationships, and accelerates R

To truly understand your SaaS company’s performance, you need to go beyond standard financial metrics, such as revenue and operating income, and dive into SaaS metrics. Debbie Rosler, Fractional CFO Read More. The post SaaS Metrics Simplified, Part One: Launch Metrics appeared first on Burkland.

Amazon, eBay and Etsy are more than household names. In the world of sales tax, they’re major marketplace facilitators. A marketplace facilitator is a platform where third-party sellers of any size and geographic area can facilitate retail sales, including the collection/processing of payments, in exchange for compensation. Think of it almost like a consignment shop.

QUESTION: Our company offers a high-deductible health plan (HDHP), and many participants contribute to their own HSAs. Several have asked about making HSA contributions on a pre-tax basis so they can receive income tax savings every payroll period (instead of waiting until they file their tax returns) and avoid paying FICA taxes on those contributions.

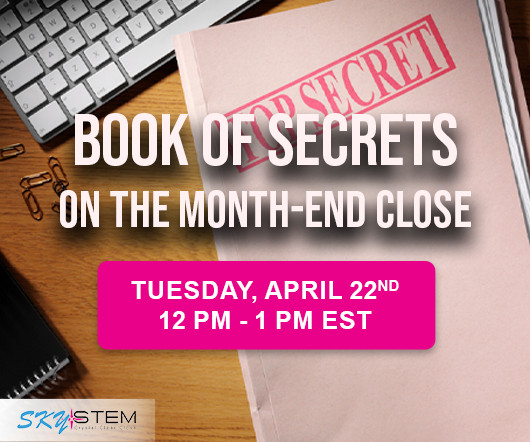

Based off SkyStem's popular e-Book, the book of secrets to the month-end close will be revealed in this one-hour webinar. Learn leading practices when it comes to building a strong and sustainable month-end close that has room to grow and evolve. Learn about the power of precise estimates, why reconciliations are critical to closing the books, how and when to automate, and how the chart of accounts play into your close process.

While Congress develops legislation that would eliminate, and/or otherwise mitigate, the current TCJA implemented state and local tax (SALT) limit on an individual taxpayer’s ability to take the itemized deduction for state and local taxes, California has just passed legislation which offers a work-around that will allow many Californians to mitigate the effects of the current $10,000 federal limitation on SALT deductions.

Many companies find themselves in return-to-work limbo, trying to determine what expectations to set for employees who have been working from home for more than a year. Making these decisions Read More. The post Is “Remote-First” the Future of Work for Startups? appeared first on Burkland.

This article was written for the Atlanta Business Chronicle Leadership Trust. To see the original post, click here. In the fall of 2020, I published an article on how the sales tax picture is changing due to COVID-19. Now that we’re over a year into the pandemic, I wanted to provide an update on the sales tax landscape, what predictions have remained the same and what’s changed.

AI is reshaping industries, yet finance remains one of the slowest adopters. Concerns over compliance, legacy systems, and data silos have made finance teams hesitant to embrace AI-driven transformation. But delaying adoption isn’t just about efficiency—it’s about staying competitive in a rapidly evolving landscape. How can finance leaders overcome these challenges and start leveraging AI effectively?

Not all businesses sell a physical product, but many businesses have inventory that is made up of materials used as a part of a service provided to a customer. In either case, these products and materials need to be accounted for in the warehouse, when they are moved to job sites, and when they are used for a client job or within the production of a larger product.

If you’re planning your estate, or you’ve recently inherited assets, you may be unsure of the “cost” (or “basis”) for tax purposes. The current rules Under the current fair market value basis rules (also known as the “step-up and step-down” rules), an heir receives a basis in inherited property equal to its date-of-death value. So, for example, if your grandmother bought stock in 1935 for $500 and it’s worth $1 million at her death, the basis is stepped up to $1 million in the hands of your gran

8 min read. With COVID hot spots once again dotting the world map and U.S officials rolling out restrictions on social distancing, business owners should be considering what they can do now to prepare for the possibility of a second COVID shutdown.

Is your tech stack working for you—or are you working for it ? 🤖 In today’s world of automation and AI, technology should simplify workflows—not add complexity. Seamless integration and interconnectivity are key to maximizing productivity, optimizing workflows, and improving collaboration. Join expert Joe Wroblewski for a practical and insightful session on how you can build a smarter, more connected tech stack that drives efficiency and long-term success!

Misclassification of employees and independent contractors is one of the most common pitfalls startups face during a due diligence process. The post Surviving Due Diligence, Part 2: Employee vs. Contractor appeared first on Burkland.

TaxConnex is proud to announce that last Sunday, August 8, TaxConnex founder and CEO, Robert Dumas, was interviewed on the Kathy Ireland show as branded content! Robert was able to highlight TaxConnex’s unique offerings to businesses looking to outsource sales tax compliance. There are still many businesses who don’t understand all the complexities surrounding sales tax or that they even have an obligation.

Finance isn’t just about the numbers. It’s about the people behind them. In a world of constant disruption, resilient finance teams aren’t just operationally efficient. They are adaptable, engaged, and deeply connected to a strong organizational culture. Success lies at the intersection of people, culture, adaptability, and resilience. Finance leaders who master this balance will build teams that thrive through uncertainty and drive long-term business impact.

If you have a parent entering a nursing home, you may not be thinking about taxes. But there are a number of possible tax implications. Here are five. 1. Long-term medical care The costs of qualified long-term care, including nursing home care, are deductible as medical expenses to the extent they, along with other medical expenses, exceed 7.5% of adjusted gross income (AGI).

What Is the Hobby Loss Rule? If your business goes too many years without making a profit, it can be classified as a hobby. When it becomes a hobby, you can no longer claim losses as business deductions. In order to determine if you are running a business or a growing hobby, the Internal Revenue Service (IRS) looks at the following qualifications: Do you put in the time to turn a profit?

Anupam Rastogi transformed his passion for building and scaling startups into a career in venture capital over a decade ago. He saw venture as a way to bring his skill Read More. The post Anupam Rastogi Shares Insights on Today’s Startup Landscape from an Early-Stage VC appeared first on Burkland.

Ever had a bad connection on a video conferencing platform? It can be a confusing and frustrating experience. That’s a lot like understanding the taxes on videoconferencing services right now. With the recent boom of video conferencing brought on by the necessity of a way to meet during the pandemic, businesses and governments alike are trying to figure out how to best apply sales tax to these services, or if they are even taxable.

In the accounting world, staying ahead means embracing the tools that allow you to work smarter, not harder. Outdated processes and disconnected systems can hold your organization back, but the right technologies can help you streamline operations, boost productivity, and improve client delivery. Dive into the strategies and innovations transforming accounting practices.

We organize all of the trending information in your field so you don't have to. Join 237,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content